October 2025 Mortgage Rates: What Homebuyers and Refinancers Need to Know

As we hit mid-October 2025, mortgage rates are showing signs of stabilization after a year of ups and downs, offering a glimmer of hope for those eyeing a home purchase or refinance. Think of mortgage rates like the weather—unpredictable but influenced by broader economic winds. Right now, they’re cooler than they’ve been in months, but will they stay that way? In this article, we’ll break down the current landscape, what’s driving these rates, and practical steps you can take to lock in a deal that fits your budget.

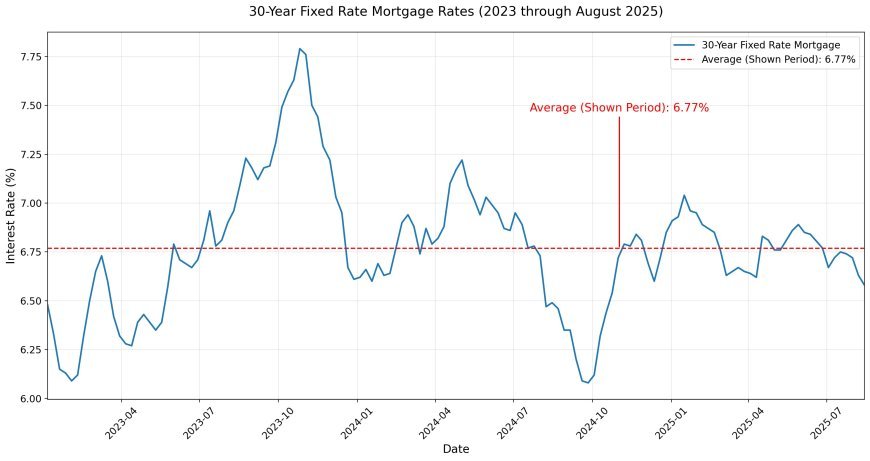

As of October 17, 2025, the average 30-year fixed-rate mortgage is hovering around 6.27%, a slight dip from last week’s 6.32%. For a 15-year fixed-rate, you’re looking at about 5.52%, down marginally from 5.53%. These figures come from Freddie Mac’s Primary Mortgage Market Survey, which tracks rates for conventional loans with a 20% down payment and strong credit.

Other sources paint a similar picture: Bankrate reports the 30-year fixed at 6.31% with an APR of 6.37%, while the 15-year is at 5.60% (APR 5.70%). NerdWallet pegs the 30-year at 6.17% APR, showing some variation based on lenders and daily fluctuations. Jumbo loans and FHA/VA options are slightly higher, around 6.37% to 6.93%, depending on the program.

These rates are the lowest we’ve seen all year, making October a potentially sweet spot for locking in—especially if you’re comparing to the 7%+ peaks from earlier in 2025.

What’s Driving These Rates?

Mortgage rates don’t move in a vacuum; they’re tied to bigger economic forces. The Federal Reserve’s recent actions are a big player here. After holding steady for most of 2025, the Fed cut rates by a quarter point in September, and another cut is highly likely at their October 29 meeting—with odds around 90% according to market tools. This isn’t a direct dial on mortgage rates, but it signals cooling inflation and boosts investor confidence, pushing rates down.

The 10-year Treasury yield, which mortgages often shadow, is sitting at about 4.1%, down from highs near 4.5% earlier this year. Economic news like jobs reports also sways things—tepid data can lower rates as investors seek safe havens like mortgage-backed securities. Add in potential government shutdown jitters, and you’ve got a recipe for steady or slightly declining rates this month.

In simple terms, it’s like a seesaw: Good economic news might nudge rates up, but uncertainty (like recession fears) tips them lower. Right now, the balance favors borrowers.

How Do October Rates Compare to Previous Months?

October’s rates are a breath of fresh air compared to the rest of 2025. Back in February, 30-year fixed rates were stuck between 6.72% and 6.95%, feeling like a heavy backpack for homebuyers. They broke below 6.5% in August after the Fed’s signals, and September saw them plunge to three-year lows around 6.30% before a slight uptick.

Year-over-year, we’re down from October 2024’s averages in the 6.5%-7% range. And forget the ultra-low 2%-3% days of the pandemic—that was a once-in-a-lifetime anomaly fueled by emergency measures. Today’s rates, while higher than those historic lows, are more normalized and could mean real savings: On a $300,000 loan, dropping from 7% to 6.3% saves about $150 monthly.

Refinance activity is picking up too, as homeowners who locked in at higher rates earlier this year see an opportunity to shave costs.

Should You Buy or Refinance Now?

Timing the market is tricky—like trying to catch a falling knife. But with rates at 2025 lows and another Fed cut on the horizon, October could be a smart window. If you’re buying, lower rates boost your purchasing power; that same $2,000 monthly payment now affords a bigger home than it did in spring.

For refinancers, the math works if you can drop your rate by at least 0.5%-1% and plan to stay put for a few years to recoup closing costs (typically 2%-5% of the loan). However, don’t wait forever—rates ticked up slightly after September’s cut, and experts warn of potential volatility if economic data surprises.

Pros of acting now: Lock in savings amid uncertainty. Cons: If rates drop further, you might refinance again (though that’s not free). Weigh your personal finances—use a mortgage calculator to run scenarios.

Tips for Securing the Best Mortgage Rate

Getting the lowest rate isn’t luck; it’s strategy. Start by boosting your credit score—aim for 740+ to qualify for prime rates. Shop around: Compare at least three lenders, as offers can vary by 0.25% or more. Consider buying points to lower your rate upfront if you plan a long stay.

Opt for a shorter term like 15 years for lower rates (and faster payoff), or explore ARMs if you expect rates to fall further—but beware of future adjustments. Finally, lock your rate when you find a good one; most locks last 30-60 days, giving you breathing room.

Analogous to budgeting: Treat rate shopping like hunting for deals on groceries—small differences add up over 30 years.

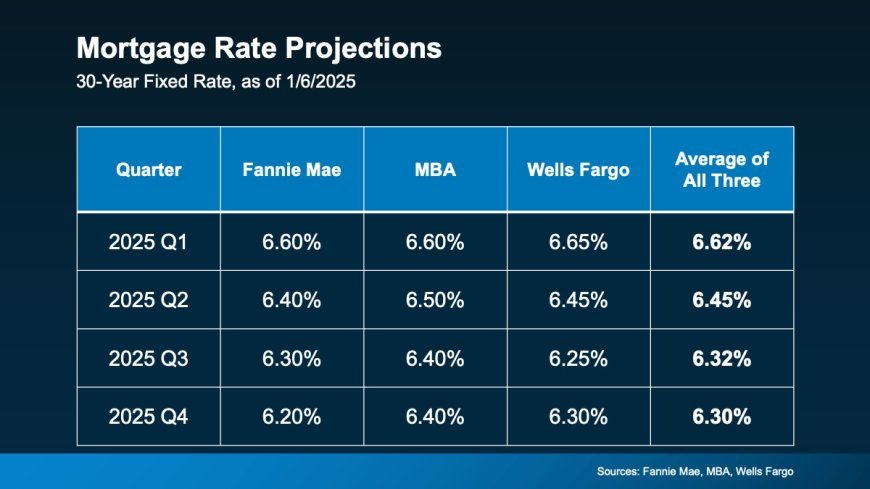

Looking Ahead: Mortgage Rate Forecast

Experts predict rates will stay in the mid-6% range through the end of 2025, possibly dipping to 6.2%-6.3% by Q4 if the Fed cuts again. Into 2026, gradual declines could continue if inflation cooperates, but don’t bank on sub-6% soon—most forecasts hover around 6.3%-6.6% for Q1 2026.

Keep an eye on jobs reports, inflation data, and the Fed’s October meeting for clues. If recession fears grow, rates could fall more; stronger economy? Expect a nudge up.

Final Thoughts

October 2025’s mortgage rates are a welcome relief in a challenging year, empowering more buyers and refinancers to take action. Whether you’re a first-timer or seasoned homeowner, focus on what you can control: Your credit, shopping savvy, and timing based on your needs—not perfection. If rates align with your goals, don’t hesitate—homeownership is about building equity, not chasing the absolute bottom. For personalized advice, consult a financial advisor or lender.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0